Something strange is happening in the US.

A rare gap has opened up between the dollar and US government debt yields as investors worry tariffs will trigger a financial crisis.

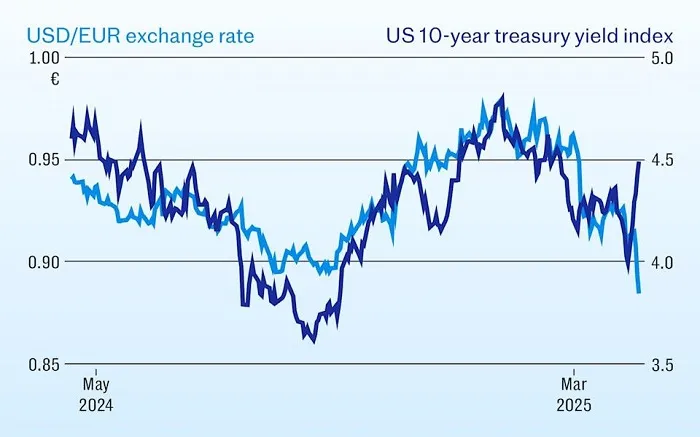

While technically that actually means the dollar is plunging while US borrowing costs are rising.

The trend has spooked investors, who have noticed that the two key financial indicators usually move in tandem, producing opposite effects.

To make matters worse, stocks have also been hammered since Donald Trump’s trade war unleashed a wave of economic turmoil.

The falling dollar and rising yields together reflect the changing fiscal position of the US, whose tariff moves put the country’s safe haven status at risk.

Christian Keller of Barclays noted that the US has been in trouble since Trump escalated the trade war earlier this month.

“The synchronized sell-off in stocks, rates and currencies is typical of emerging markets, but not for the world’s core safe haven markets,” he said.

Investors have become accustomed to the idea that the US is the best place for their money in boom or bust, giving it the “exorbitant privilege” of controlling the world’s reserve currency.

That meant lower borrowing costs and easier access to large amounts of foreign money to invest in the U.S., making the country richer and helping its economy grow faster.

But suddenly, investors began to abandon the U.S., dumping the dollar and other assets at the same time.

It represented a stunning reversal of usual behavior, breaking what was seen as a cardinal rule of global finance.

The result was a sharp divergence in the dollar and bond yields, which generally tend to move in tandem.

Even as the president suspended his toughest tariffs on nearly every country except China, markets haven’t complied.

Since April 2, which Trump called “Liberation Day,” the dollar has fallen more than 4% and the 10-year Treasury yield has risen to 4.5% from 4.2%.

Keller said the moves broke with historical norms.

“The dollar’s depreciation due to higher U.S. tariffs (contrary to textbook economics theory), and the sell-off in Treasuries and the decline in equities (contrary to risk aversion) are more broadly revealing dynamics triggered by Trump’s tariffs,” he said.

Investors no longer trust the U.S.

As tariffs hurt imports, textbook economics would suggest that the dollar would strengthen. Similarly, expectations of a recession should push down interest rates, including bond yields.

But the opposite has happened, for a simple reason: investors no longer trust the U.S.

“Rising Treasury yields are due to foreign holders demanding a higher term premium to compensate for concerns about Treasuries as a worry-free haven,” Keller said.

Netwealth economist Gerard Lyons noted that the U.S.’s dominance over the past 25 years stems in part from a lack of alternatives.

For example, the German mark was replaced by the euro, resulting in the disappearance of a safe haven, and Japan is no longer seen as the robust market it once was.

In addition, several pillars that have supported bonds in recent years have been kicked off.

Quantitative easing (QE), which pushed the Fed’s asset purchases to a peak of nearly $9tn (£6.9tn), has long since disappeared as the Fed’s balance sheet has shrunk.

When the policy was at the heart of central bank operations after the financial crisis, a new round of QE would push down the dollar while pushing down yields, thereby reducing borrowing costs.

The dominance of US stocks has also affected the dollar’s performance, as the so-called “Big Seven” have poured money into the US. But that dominance has also been hit by the trade war.

Meanwhile, the US trade deficit stems from US companies and households buying goods from abroad.

This leaves dollars in the hands of foreigners, especially Japan and China, who in turn reinvest them in the US by buying US government bonds.

Currently, more than a fifth of the US government’s $36tn debt is financed by overseas buyers.

If Trump succeeds in eliminating the US trade deficit, he will also cut off the flow of dollars back into the US bond market.

Crucially, there are limits to what the authorities can do to restore confidence in the US economy.

For example, Fed Chairman Jerome Powell could buy bonds to prop up markets.

But he would be hard-pressed to start QE again because of concerns that it could reignite inflation along with tariffs.

‘Liz Trump moment’

More importantly, the Fed can’t limit the impact of Trump’s erratic policymaking, said Krishna Guha of Evercore ISI, who described the recent sell-off as “almost unprecedented”.

“By supporting liquidity, the Fed can limit price overshoots,” he said, “but it can’t stop capital outflows caused by a loss of confidence in U.S. economic policymaking.”

Ultimately, the reserve currency status that gives the U.S. such global influence is built on trust. And once that trust is questioned, it risks becoming a self-fulfilling prophecy.

Holger Schmieding of Berenberg Bank warned of a possible “Liz Trump moment” in the U.S., with the former prime minister’s mini-budget sparking market chaos.

“Unconventional policies that risk a country’s public finances and growth prospects could cause bond investors to question the assumption that government debt is risk-free,” he said.

“The breakdown in the relationship between Treasury yields and the dollar highlights investor concerns about Donald Trump’s policy agenda.”

“The damage from the trade war could accelerate the deterioration of the US fiscal position.”

“The huge uncertainty will lead to a contraction in investment and consumption, driving a sharp slowdown in the US economy.”

He predicts the dollar will fall further, yields will rise, and the striking divergence between these key economic indicators will worsen.

“These developments are very important because they suggest a paradigm shift in the perception of the United States as a destination for capital flows,” said Barclays’ Keller.

“This is not only triggered by extreme tariff policies, but also the related concept of charging the rest of the world for the dollar as a reserve currency.

As tariffs and foreign policy proposals become increasingly radical, these ideas are also starting to look less far-fetched. This in turn requires the rest of the world to reconsider the United States as an investment destination.