Even as the company’s stock price fell sharply and the freight market failed to support Triumph Financial’s profitability, CEO Aaron Graft still claimed milestones and said the company’s product pricing would take new aggressive measures.

In his quarterly letter to investors released alongside the company’s earnings report on Wednesday, Graft said Triumph’s “network participation” (the proportion of forwarded freight touched by one or more of its payment systems) exceeded 50% for the first time in the first quarter. The company has maintained steady momentum on the road to that number; from the first quarter of last year to the end of 2024, Triumph’s first four quarters of participation were 42.7%, 46.6%, 47.8% and 48.7%, respectively.

However, after two consecutive quarters of positive earnings before interest, taxes, depreciation and amortization (EBITDA), Triumph’s payment division’s margin slipped to a negative 0.1%. Graft said in the letter that several non-core expenses in the division led to the EBITDA deficit.

That hasn’t stopped Triumph from pricing its payments products more aggressively, Graft said.

Network monetization

“Now is the time to shift more focus to monetizing the network” — “the network” referring to the complete invoice audit and payment system that is at the heart of Triumph’s growth plan.

“We are committed to monetizing payments with the goal of pricing our services fairly and consistently based on the value we create for our customers while continuing to generate revenue,” Graft said. Many existing customers can trace their roots back to Triumph’s acquisition of HubTran in 2021, which kicked off the growth of the audit network, but their fees haven’t kept up. “The value we’re creating for many of our customers has been growing faster than our pricing,” he said.

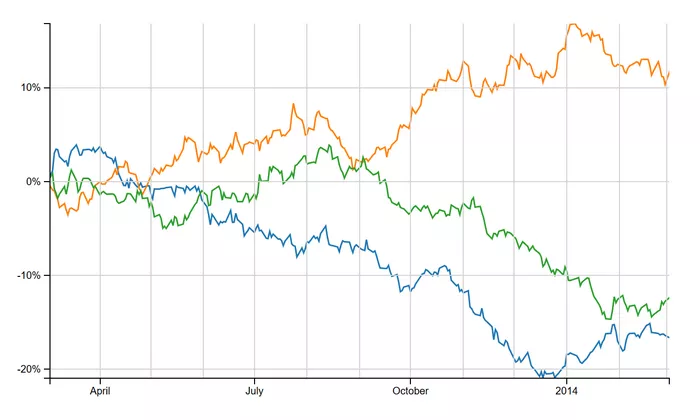

Triumph’s stock has been hammered in recent months. It’s down 34.4% year to date, and a whopping 45.6% in the past three months. Graft acknowledged the share price drop without disclosing specific numbers, but said: “Seasonal and cyclical factors intertwined with trade policy uncertainty and recession fears, [and] our business valuation has been impacted.”

But in a recurring comment this quarter, Graft also said earlier statements that “the plan is to stick to the plan… has not changed.”

“We will not blame freight markets and trade policy for our performance, nor will we let them hinder our strategic vision,” he said. “We could have deviated from the plan, stopped additional investment, postponed immediate restructuring charges, or cut costs to achieve modest profitability in the quarter. There would have been a cost to either executing or avoiding these. We will not compromise long-term value to avoid current pain.”

Greenscreens Plan

Graft’s letter is the first since Triumph acquired Greenscreens.ai, an analytical pricing tool that is now at the core of Triumph’s intelligence unit. Triumph is expected to continue to develop the unit and incorporate other data generated by its payments and factoring businesses.

“Because we transmit and audit more data for payments than anyone else, we have the densest and cleanest data set on the market to build rating products from,” Graft said. “We also have the customer relationships and integration resources to accelerate our go-to-market strategy. That’s why we chose this path and why we’re determined to stay the course.”

Greenscreens’ gross margins are about 90%, Graft said. The deal is expected to close this quarter.

LoadPay, designed for small and medium-sized operators, is now live. LoadPay aims to get money into its bank accounts faster. In the first quarter, operators received $5 million in payments into their LoadPay accounts, $3.2 million of which occurred in March. Triumph currently has more than 1,000 LoadPay accounts and expects to reach 5,000 to 10,000 by the end of the year.

While LoadPay is still in its infancy, Graft made it clear that its plans are ambitious. The company’s factoring business has long been a cornerstone of Triumph’s business and will have a “symbiotic” relationship with LoadPay as both work to get money into drivers’ hands faster.

But Graft sees greater potential in LoadPay. “The interchange revenue we achieve with LoadPay is higher than the discount rates we charge in factoring,” he said. “LoadPay is a more efficient business model that generates higher margin revenue.”

He said factoring is still valuable, but Triumph now sees it more as “part of a larger product suite.”

Graft also made the following points in his letter:

Earnings were impacted by expenses related to LoadPay and the company’s “factoring as a service” product, which is designed to assist third-party customers with back-office factoring operations. But revenue from these products is just beginning to have an impact on the company’s earnings. Graft also said CH Robinson (NASDAQ: CHRW) is the first customer for the “factoring as a service” product.

The average invoice value for Triumph coverage was $1,769, just $2 higher than the previous quarter and $2 lower than the same period last year. However, average diesel prices rose 9-10 cents per gallon this quarter, according to weekly data from the U.S. Department of Energy/Energy Information Administration (EIA), which should push average invoice values higher. Graft’s letter published for the first time the average rate per mile of dry trucks in its coverage invoices. In the first quarter, the rate was $2.05, up from $2.02 in the previous quarter. It was $1.98 in the previous two quarters.

Graft’s letter was decidedly negative about the market. One thing it specifically called out: contract rate declines. “The more rapid decline in average invoice values in 2025 put more pressure on contract rates than spot rates. For the first time in the past three years, we experienced a decline in contract rates relative to spot rates. Contract rates declined 7%, while spot rates declined 5%.